Everyone Is Asking the Wrong Question About Hyperscalers and the Iran War

The energy cost story is a red herring. The real risk is sitting in a data center in Bahrain.

There is a question bouncing around finance Twitter right now that goes roughly like this: “Oil is at $110. Natural gas is spiking. Doesn’t this crush hyperscaler margins?”

It’s a reasonable question. It’s also the wrong one.

And the fact that everyone is asking it — rather than the much more uncomfortable question that follows from reading a few 10-K filings — is the kind of thing that happens when investors confuse the thing they’re worried about with the thing they should be worried about.

So let me tell you what I actually think is happening.

The Energy Cost Story Doesn’t Hold Up

Start with the data, because it matters here. WTI crude is trading around $106 and Brent at roughly $108, up something like 50% since the US-Israel strikes began on February 28. The headlines are dominated by $110 oil, $115 oil, analysts at Kpler floating a scenario where Brent hits $150 by end of March if the Strait of Hormuz stays effectively closed.

But here’s the thing: data centers don’t run on oil. They run on electricity. And the fuel that generates most of that electricity in the US is natural gas — priced at Henry Hub, which is a domestic market largely insulated from what happens in the Persian Gulf.

Natural gas rose about 11% last week to roughly $3.33 per thousand cubic feet. That’s real. That’s not nothing. But it’s not 50%. And even that 11% overstates the actual cost exposure for Microsoft, Amazon, and Google, because a substantial portion of their US power is locked up in long-term Power Purchase Agreements that were signed at pre-war prices. The spot market is not their market — or at least not for the majority of their US capacity.

So when you model through the actual transmission mechanism — oil spike → domestic gas prices → wholesale electricity → data center OPEX — what you find is that the US operations of the hyperscalers are reasonably well-buffered. Not immune, but buffered. The energy cost story for US infrastructure is, at current nat gas prices, more noise than signal.

Europe is a different story. European natural gas prices have risen more sharply than US prices, because European markets are more directly linked to global LNG pricing and Gulf supply chains. Hyperscalers with large European data center buildouts — which is all of them, given GDPR and data sovereignty requirements — face more direct pass-through. That’s worth watching. It’s just not the main event.

The Main Event Is a Different Map

Here is the question I think you should be asking instead: which hyperscaler has production infrastructure running inside the war zone right now?

The answer is: all of them.

AWS operates an active region in Bahrain — me-south-1, launched 2019, designed for Middle East cloud workloads. Microsoft Azure has two production regions in the UAE — UAE North (Dubai) and UAE Central (Abu Dhabi). Google Cloud has infrastructure in the Gulf as well, including Qatar. These aren’t edge deployments or experimental capacity. They’re production availability zones serving enterprise customers across the Middle East.

And Dubai International Airport was damaged by Iranian drone strikes on the second day of the conflict. Iranian missiles and drones have targeted Qatar, Bahrain, Kuwait, and the UAE in barrages throughout the past ten days. A Bahraini oil refinery was hit and caught fire. The UAE and Qatar — where Azure and Google have real infrastructure — are not observing this conflict from a distance. They’re in it.

Now. Have any of the three companies disclosed a material disruption to Gulf region services? Not as of this writing. Availability dashboards have shown no major reported outages. It’s possible — likely, even — that Gulf region data center operations are continuing with backup power and modified logistics. Hyperscalers build for five-nines uptime; they have diesel generators and redundant connectivity precisely for moments like this.

But here’s what strikes me as worth sitting with: the market is pricing the Iran war as an energy cost story for these companies, when the more acute short-term risk is infrastructure continuity in a war zone.

The Diesel Problem Nobody Is Talking About

There’s a secondary cost story that is real and immediate, and it’s not natural gas. It’s diesel.

Diesel is now selling for about $4.60 a gallon — up roughly $0.83 in a single week. That matters for data centers specifically because backup generators run on diesel, not natural gas. Every major facility has thousands of gallons of diesel reserves and ongoing fuel contracts. In a prolonged disruption, the cost of maintaining backup generation readiness goes up in a way that isn’t hedged by PPAs.

This isn’t an existential cost item for Microsoft or Amazon. But it shows up in OPEX and it’s correlated with the duration of the conflict, not just the spot price of nat gas. The longer this goes on, the more it matters.

The Construction Pipeline Is the Longer Game

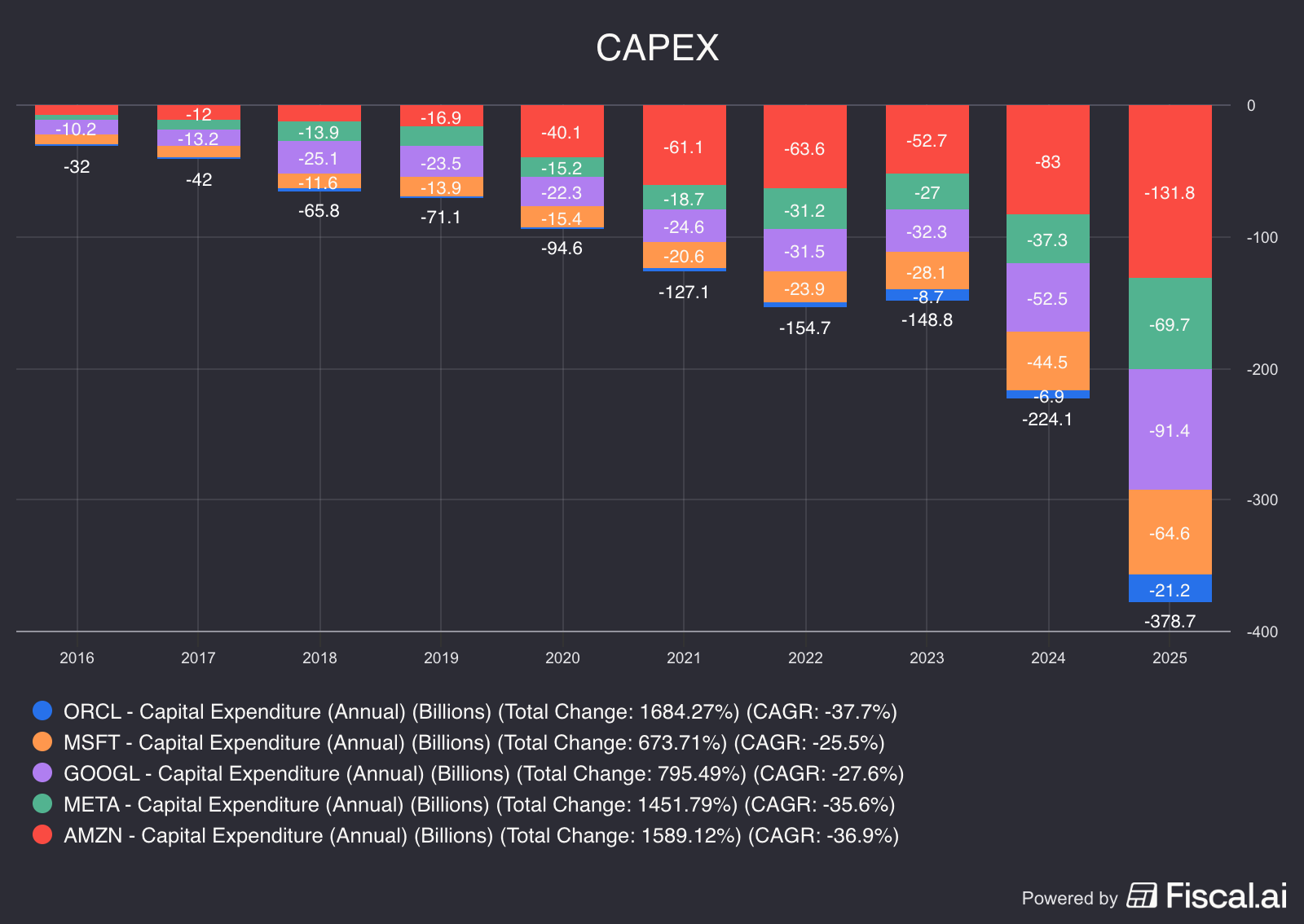

Step back from the quarterly OPEX question and look at CapEx timelines, because that’s where I think the real financial story is.

Step back from the quarterly OPEX question and look at CapEx timelines, because that’s where I think the real financial story is. These five companies — Amazon, Alphabet, Microsoft, Meta, and Oracle — spent a combined ~$379 billion on capital expenditure in 2025 alone. Amazon put in $131.8 billion. Alphabet $91.4 billion. Microsoft $64.6 billion. Meta $69.7 billion. Oracle, the newcomer to this conversation, nearly tripled its spend to $21.2 billion in a single year. For reference, Microsoft’s entire CapEx budget in 2016 was $8.3 billion. The AI infrastructure buildout isn’t a future commitment — it’s already happening at a scale that makes every prior tech investment cycle look like a rounding error.

Every dollar of that spend requires diesel-heavy logistics for construction, copper (up alongside oil in the risk-off environment), steel, and — most critically — specialized electrical transformers that are already on 18-24 month lead times in normal conditions.

A sustained $100+ oil environment does not torpedo these projects. But it adds inflationary pressure to supply chains that were already stretched. Project costs go up. Timelines extend. And in a world where AI infrastructure spend is one of the few things holding equity valuations for these companies together, any signal that the CapEx timeline is slipping is going to be read as a negative AI demand signal.

That’s the second-order effect that I think the market will eventually price, if the conflict extends into Q2.

What Would Change My Mind

I think the market is under-pricing Gulf infrastructure risk and correctly pricing US energy cost risk. But I want to be honest about where I could be wrong.

If AWS, Azure, or Google Cloud report a material service disruption in their Gulf regions before the end of March — and the market’s reaction is contained — then I’m wrong about investor pricing. The market will have told me it doesn’t care about Gulf infrastructure continuity, and I’ll need to reconsider whether this is actually an undisclosed risk or just a regional revenue rounding error.

Separately, if Henry Hub gas prices breach $5.00/mcf by mid-April, the energy cost transmission becomes material enough to show up in Q1 2026 earnings guidance. At that point the question everyone is already asking becomes the right question. I’d look for that in any hyperscaler earnings calls between April and June — specifically whether any company revises power cost assumptions in forward guidance.

Until one of those two things happens, I think the energy-cost framing is a distraction.

Where I Land

The Iran war is bad for hyperscaler stocks — but mostly for macro reasons, not fundamental ones. S&P 500 and Nasdaq futures are down 1.6-1.9% this morning on risk-off sentiment, inflation concerns, and general “oh no, a war” repricing. That’s a valuation multiple problem, not a business model problem. For US data center operations, the PPA buffer and Henry Hub/crude decoupling mean actual OPEX impact is manageable at current prices.

But I’d be watching the Gulf region infrastructure story more carefully than the headlines suggest. The fact that hyperscalers have live production regions in Bahrain, UAE, and Qatar, and that the market has barely mentioned this in the energy cost conversation, feels like the kind of gap that closes fast if something actually goes down in one of those facilities.

Anyway. The energy cost story is real in Europe and for diesel, and worth a modest negative adjustment to near-term numbers. The Gulf infrastructure story is potentially larger and almost entirely unpriced. I hold positions in MSFT, AMZN, and GOOGL — I’m not reducing on energy cost fears, but I’m watching the availability dashboards for Gulf regions with more attention than I usually would.

What to Watch

[March–April 2026] → AWS me-south-1 and Azure UAE availability dashboards → Any reported degradation in Gulf region services would validate the infrastructure risk thesis and likely trigger a re-rating of this as a disclosed risk item.

[April 2026 earnings calls] → Management commentary on power cost assumptions → If any hyperscaler revises Q1 or full-year power cost guidance upward, the energy cost story becomes a real number, not a transmission mechanism question. Watch for language around “energy cost headwinds” or PPA coverage ratios.

[End of March 2026] → Henry Hub nat gas vs. $5.00/mcf → Eurasia Group flagged that LNG prices will keep climbing until Hormuz shipping resumes. If US nat gas follows European gas higher and breaks $5, the cost buffer shrinks materially.

[Any day, ongoing] → Strait of Hormuz reopening signals → The oil and diesel cost story is entirely about Hormuz. A credible reopening announcement — ceasefire, US naval escort program, whatever — would immediately release pressure on diesel and European gas prices and remove the clearest tail risk.

[Q2 2026 filings] → Gulf region risk factor disclosures → Watch whether MSFT, AMZN, and GOOGL add language around geopolitical risk to their Middle East infrastructure in their 10-Qs. If they do, it signals internal recognition of a previously undisclosed risk. If they don’t, either nothing happened or the legal review didn’t flag it — both useful signals.

Nothing in this post is investment advice. This is financial analysis and opinion for informational purposes only. I hold positions in MSFT, AMZN, and GOOGL as part of a diversified portfolio. All data as of March 9, 2026.